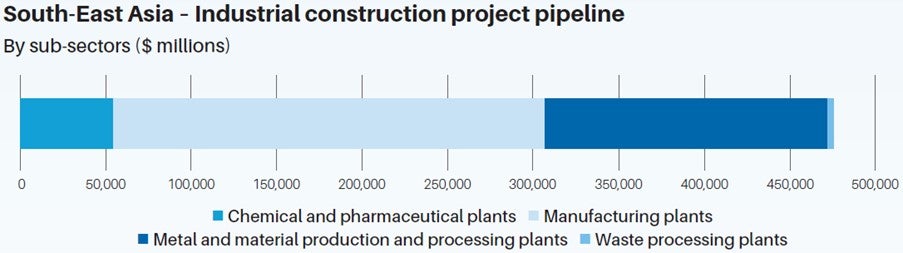

South-East Asia

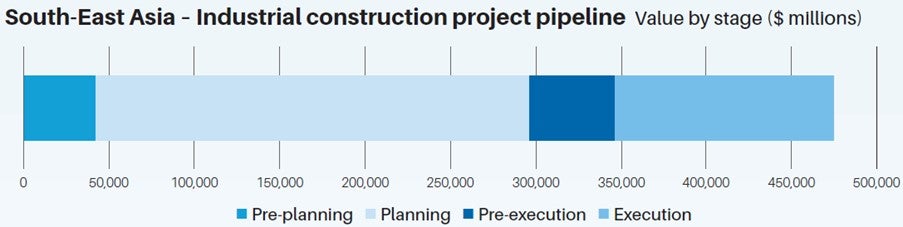

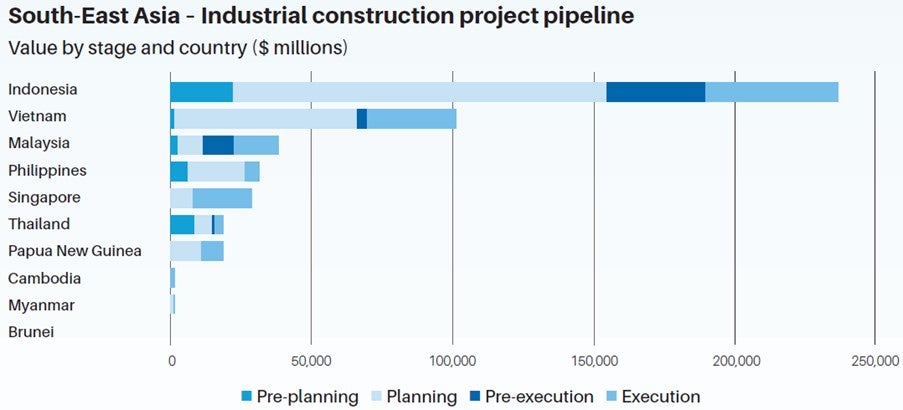

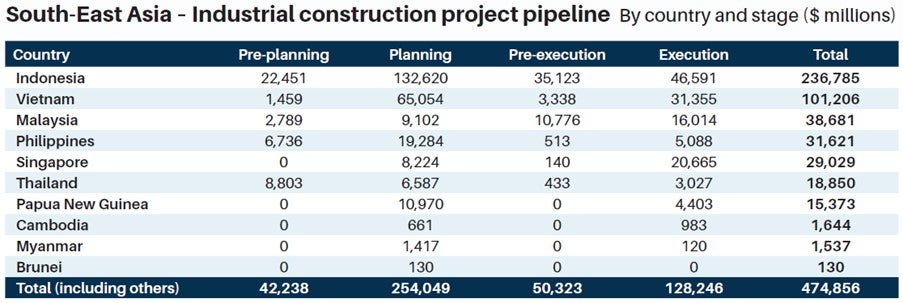

The industrial construction pipeline of projects in South-East Asia is valued at a total $474.9bn, with Indonesia at an estimated value of $236.8bn in the pipeline, a share of 49.9%. Countries such as Vietnam and Malaysia also have relatively high project pipelines, valued at $101.2bn and $38.7bn, respectively.

In Indonesia, the government is implementing new incentives to boost production, particularly in the electric vehicle (EV) sector. The government aims to become one of the world’s top three producers of EV batteries, targeting a production capacity of 140GWh per annum by 2030.

In January 2025, Hong Kong-based battery manufacturing company REPT Battero announced its plan to invest $139.5m to build a new battery production facility in Indonesia. The production plant is expected to produce lithium-ion batteries, modules and packs for both electric vehicles and energy storage systems, with an annual production capacity of 8GWh. According to the Ministry of Investment and the Indonesia Investment Coordinating Board (BKPM), foreign direct investments (FDI) in the country rose by 12.7% YoY in Q1 2025, reaching $13.7bn. The mining sector attracted more FDI compared with other sectors, attracting $6.5bn.

In Vietnam, the Ministry of Construction is planning to implement a major reform to simplify administrative procedures and improve the business environment for the construction industry in 2025. According to the Foreign Investment Agency (Ministry of Finance), the total FDI realised in the country grew by 7.2% in Q1 2025, reaching $5bn, of which the processing and manufacturing industry accounted for $4.1bn in Q1 2025.

North-East Asia

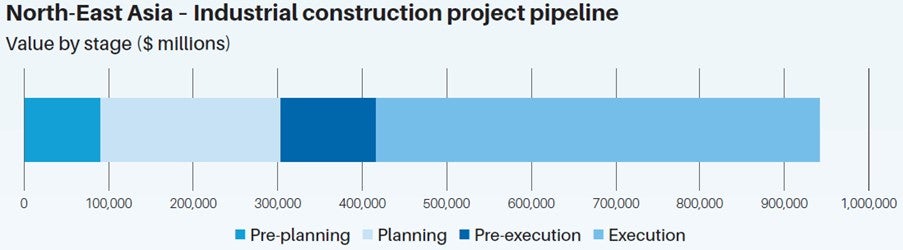

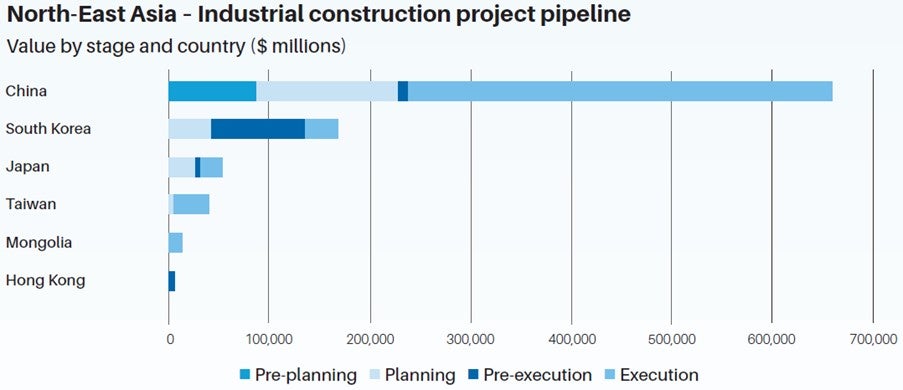

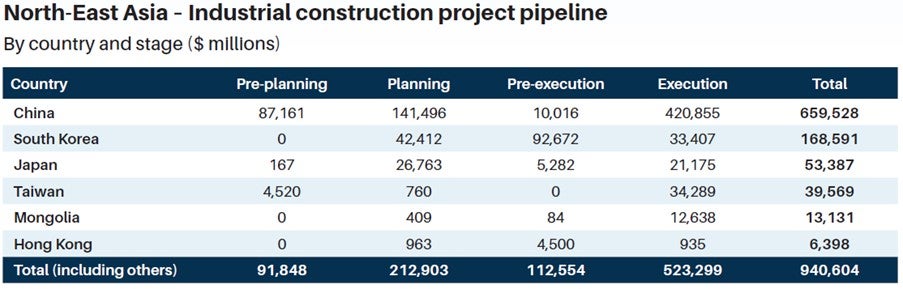

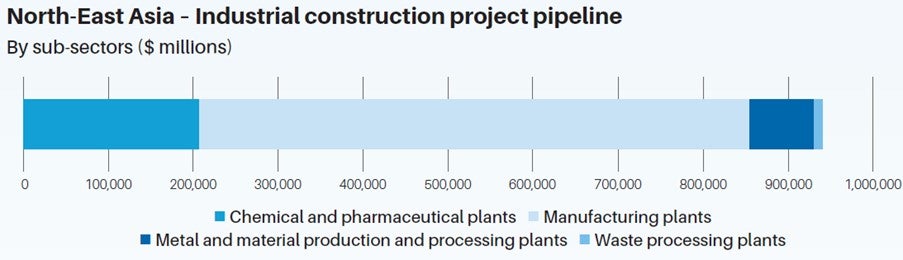

North-East Asia’s industrial growth is largely innovation-driven in tech-orientated sectors. Semiconductors and EV production plants make up a large proportion of the project pipeline. The region’s project pipeline totals $940.6bn, which accounts for approximately 18.6% of the overall global pipeline value, of which China’s industrial construction projects are estimated at $659.5bn or 70.1% of the region project pipeline, by value.

China’s renewed focus on innovation and self-reliance has driven an uptick in investment in semiconductor manufacturing plants. In March 2025, Jiashan Nanxin Semiconductor Technology (JNST) announced its plan to develop a major chip testing industrial park in Jiashan County, Jiaxing City. The project will be implemented in two phases on a 2ha site. The first phase will be developed by Q3 2032, while the second phase will be developed by Q3 2035. The project reflects China’s ongoing push to bolster its semiconductor capabilities and reduce reliance on foreign technology in critical sectors.

In April 2025, a new law aimed at boosting confidence in the private sector while strengthening the Chinese government’s role in China’s economy was passed amid heightened trade tensions with the US. Effective from May 2025, the new law hopes to encourage fair competition, improve legal protections and promote innovation within private businesses. However, the ongoing US-China trade tensions are expected to significantly impact China’s trade relations, as well as short to medium term investment and economic growth.

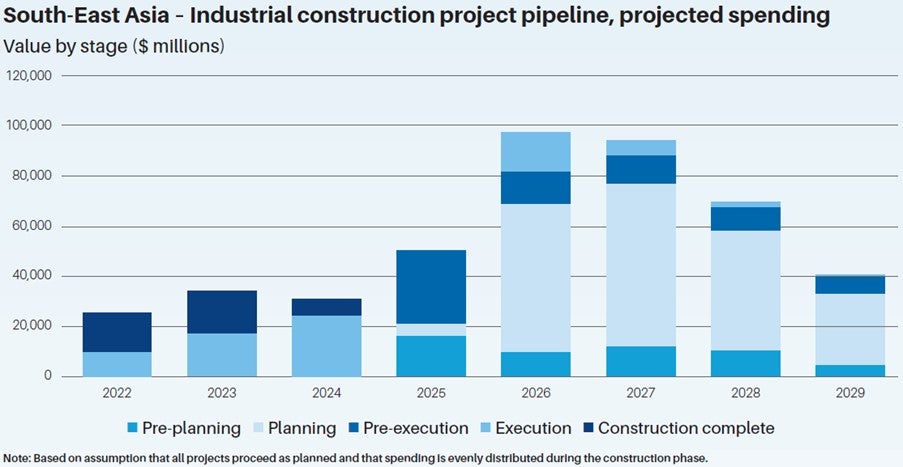

- In South-East Asia, current industrial projects are valued at $474.9bn according to GlobalData’s tracking, including projects from announcement to execution stages. The region’s overall pipeline is relatively less developed, with 62.4% of projects in the pre-planning, totalling $296.3bn. If we assume that all projects move ahead as scheduled, spending will increase from $49.9bn in 2025 to $97.6bn in 2026.

- The largest project under way in this region is the $28bn Tanah Kuning Industrial Park Integrated Ferronickel Complex project, currently in the planning stage. Tsingshan Holding Group (THG) is planning to build an integrated ferronickel complex in North Kalimantan, Indonesia. The project requires the construction of a ferronickel smelter with a capacity of 1.5MTPA, a stainless steel production facility with a capacity of 2MTPA, a carbon steel production facility with a capacity of 10MTPA, a ferromanganese production facility with a capacity of 500,000TPA, a ferrosilicon production facility with a capacity of 200,000TPA, an aluminium production facility with a capacity of 1MTPA, a ferrochrome production facility with 1.2MTPA, and a 5,000MW hydroelectric power plant, which will supply power to the complex, as well as the installation of machinery and equipment, safety and security systems.

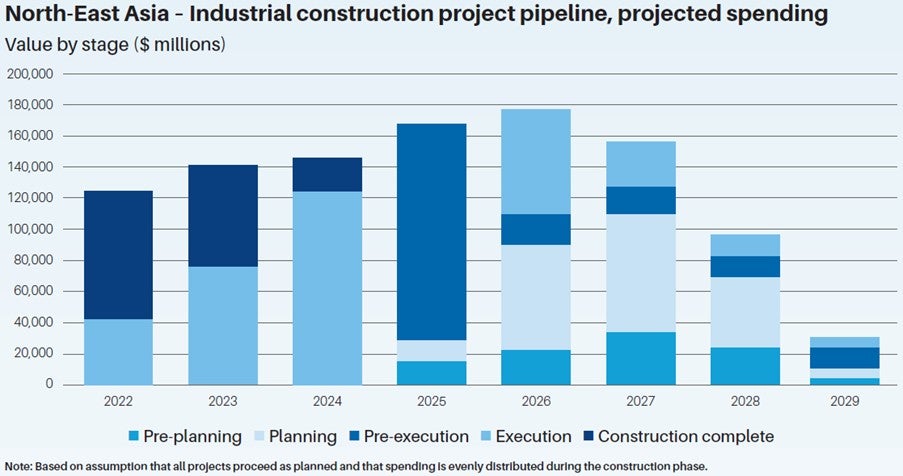

- According to GlobalData, North-East Asia industrial construction projects have been tracked to a total value of $940.6bn, which includes projects from announcement to execution stages. The region’s overall pipeline angles towards the late stage, with pre-execution and execution stage projects accounting for 67.6% of total projects, equalling $635.9bn in value. If all projects move ahead as planned, spending is projected to grow from $167.6bn in 2025 to $176.7bn in 2026, before slowing down to $156.2bn in 2027.

- The $92bn Yongin Semiconductor Industrial Cluster project in Gyeonggi-do, South Korea, is highest value project in the pipeline, which includes the construction of four semiconductor fabrication plants (FABs). Construction is expected to begin in Q2 2025 and to be completed in Q2 2032.