Western Europe

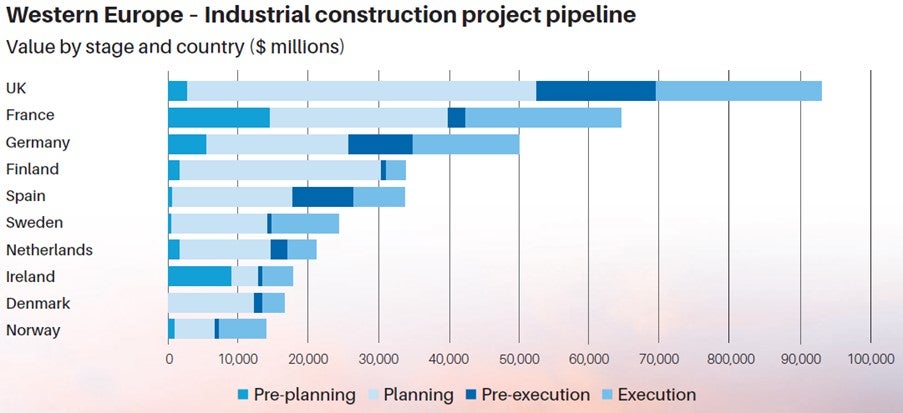

In Western Europe, the industrial construction project pipeline is valued at $408.4bn, supported by major industrial development plans across the region. The UK and France lead the way, with both countries respectively accounting for 22.8% and 15.8% of the region’s project pipeline. In the UK, the government’s investment under the Auto2030 programme is set to bolster industrial construction, with a planned strategic investment of $2.6bn in the automotive industry by 2030.

In February 2025, the UK government announced its plan to boost the UK steel manufacturing sector through its $3.2bn support package. In another positive development for the sector in May 2025, the UK and India signed a free trade agreement, which will make it easier for UK companies to export goods to India, supporting industrial construction in the country.

Moreover, semiconductor shortages have highlighted the need to increase investment in domestic production to become less dependent on foreign supply chains. The EU signed its Chips Act in early 2023, which will direct $46bn into semiconductor production.

Individual EU member states are also investing heavily in EVs, high-tech and green manufacturing. In February 2025, the Japanese battery cell manufacturer Automotive Energy Supply Corporation (AESC), revealed that the EU approved a grant of $51.1m for its $1.4bn battery plant in Douai, France. This involves the construction of a manufacturing plant that produces lithiumion cells and battery modules, developing in phases by 2030.

Eastern Europe

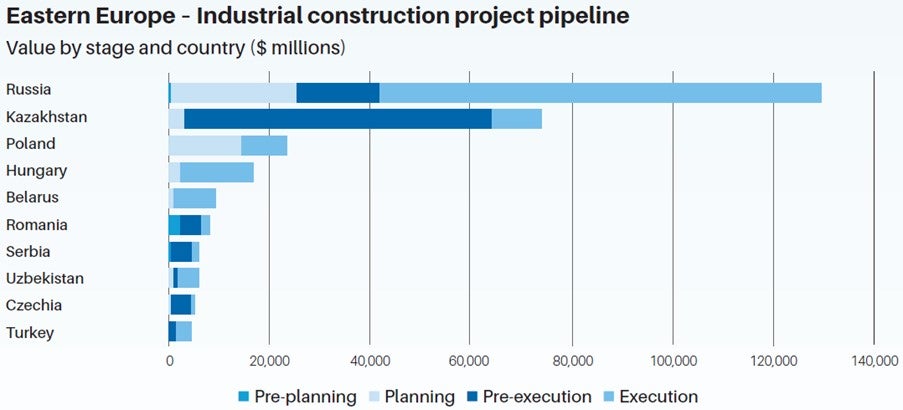

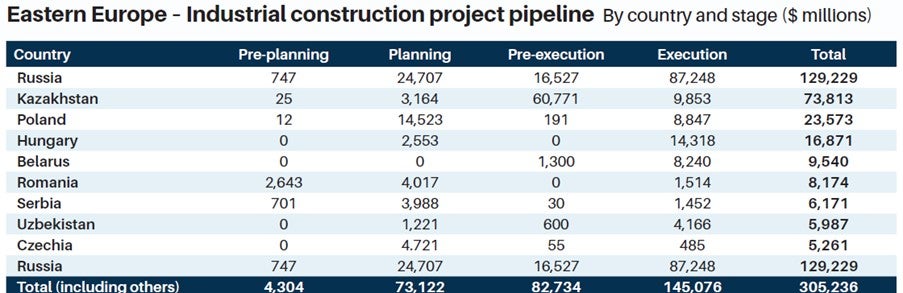

The Eastern European project pipeline for industrial construction amounts to $305.2bn, which Russia alone accounts for $129.2bn. Russia, Kazakhstan and Poland, as the three largest markets in the region, collectively accounting for 74.2% of the regional project pipeline by value. However, a lot of industrial projects in Russia have been postponed or cancelled since the start of the conflict in Ukraine. The Russian industrial construction market is also expected to encounter challenges owing to an increase in capital allocation towards the defence sector and the effects of Western sanctions on exports. In late-February 2025, the EU released its sixteenth package of sanctions against Russia, which includes a ban on the import of primary aluminium by 2026. This package also includes a ban on the export of technologies and software to Russia for usage in oil and gas exploration works.

Despite Western sanctions, the country’s manufacturing sector has continued to grow, owing to investments in defence-related manufacturing and in development of special economic zones (SEZ). In January 2025, the Ministry of Economic Development announced that the construction work of the Khakass Technological Valley SEZ in Khakasiya is scheduled to receive approval in September 2025. Additionally, the government’s focus on investing $2.5bn in the semiconductor industry by 2030 is expected to support the sector’s output. To boost the demand for the auto sector, in January 2025 the Ministry of Industry and Trade announced its aim to invest $611.8m to provide subsidised car loans that will boost auto manufacturers’ ability to expand their manufacturing units.

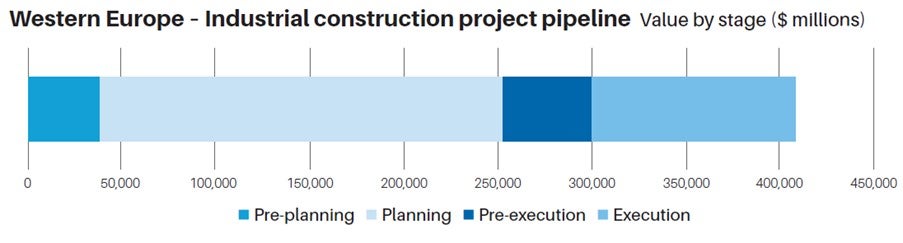

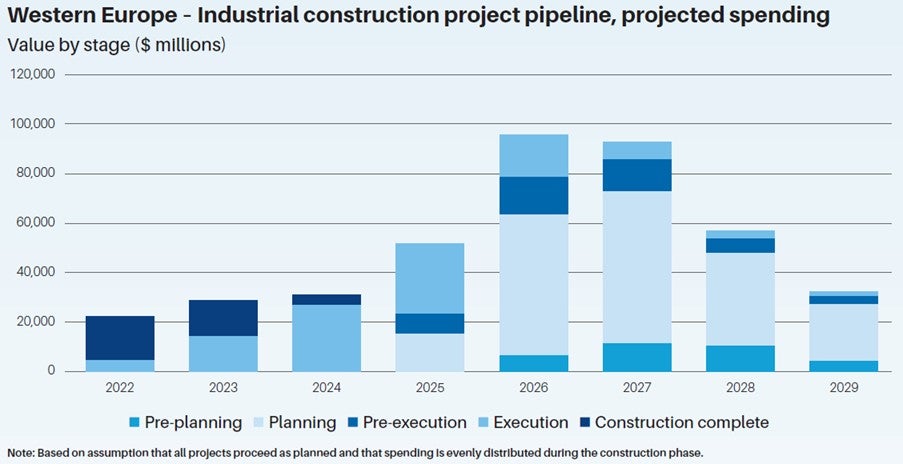

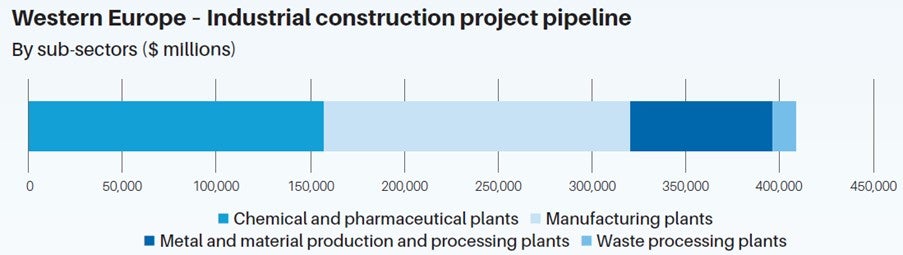

- GlobalData is currently tracking industrial construction projects in Western Europe with a total value of $408.4bn, which includes projects from announcement to execution stages. The overall pipeline in Western Europe is skewed towards projects in the earlier stages, with those in the pre-planning and planning stage accounting for 62% of projects, totalling $253.4bn in value. Assuming all projects move ahead as planned, spending will peak in 2026 at $96.3bn, with $51.9bn expected spending for 2025 in Western Europe.

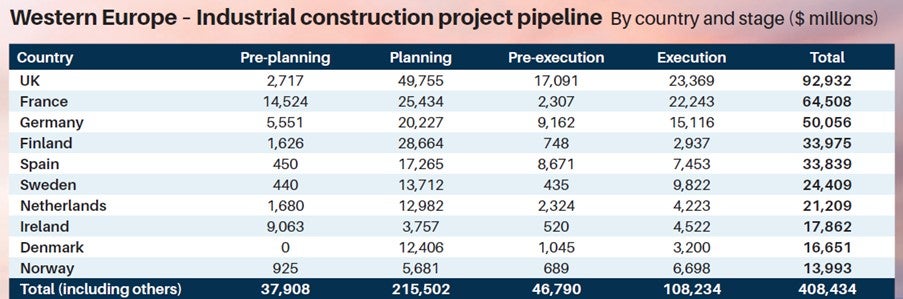

- The UK is the largest country in the Western Europe region, accounting for 22.8% of the regions pipeline, by value, at $92.9bn. France and Germany follow, with 15.8% and 12.3% of the region’s total project pipeline at $64.5bn and $50bn, respectively.

- The largest project in the pipeline is the $15bn Sellafield Plutonium Recycling Plant project, which is in the planning stage and involves the construction of a plutonium recycling plant in Cumbria, England. The project also includes the construction of a new MOX fabrication facility, plutonium storage facilities, a substation, a waste disposal facility and installation of reactor coolant pumps.

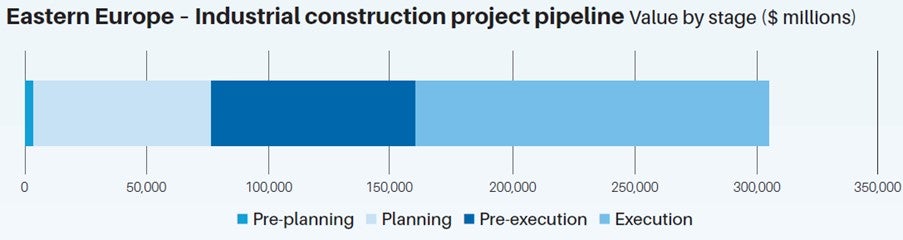

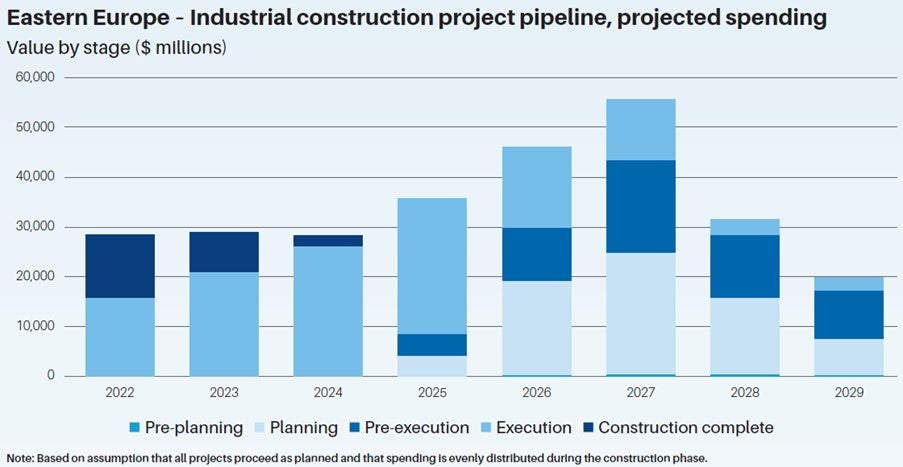

- GlobalData is currently tracking industrial construction projects in Eastern Europe with a total value of $305.2bn, which includes projects from announcement to execution stages. The overall pipeline in Eastern Europe is skewed towards late-stage projects, with projects in the pre-execution and execution stages accounting for 74.6% of projects, totalling $227.8bn in value. Assuming all projects move ahead as planned, spending will rise from $35.8bn in 2025 to $46bn in 2026 and $55.5bn in 2027.

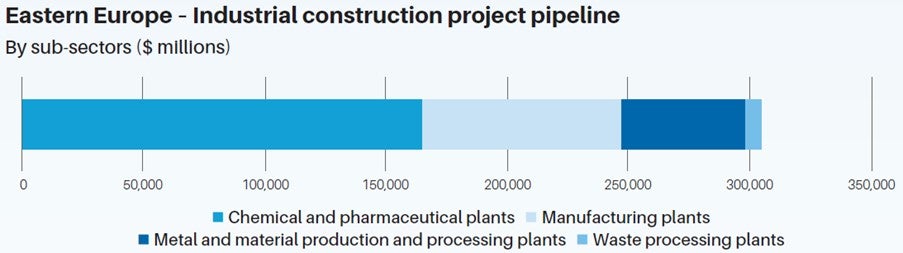

- Svevind’s $54.1bn green hydrogen production plant in the Mangystau region of Western Kazakhstan in the largest in the region’s pipeline. The project involves the construction of a 20GW green hydrogen plant, a desalination plant with a capacity of 255,000m3 per day, and a 40GW renewable energy station (wind and solar).