Many countries in the Middle East and North Africa (MENA) rely heavily on finite natural resources like oil and gas, while lacking a large manufacturing base. Although current oil and gas prices are high, long-term trends suggest a potential decline, prompting regional efforts to diversify economic capabilities. Saudi Arabia and Oman are at the forefront of this transformation, together accounting for 44.8% of the region’s industrial project pipeline.

Oman’s Vision 2040 initiative targets a significant expansion of the country’s industrial zones and a more robust manufacturing base, from 11 to 16 by 2040. Saudi Arabia is also pursuing industrial development as part of its efforts to position itself as a global hub for critical minerals and mining by 2030, announcing in January 2025 a $100bn minerals project with $20bn already in advanced stages. Additionally, the country launched a $2.7bn industrial incentives programme to support various manufacturing ventures.

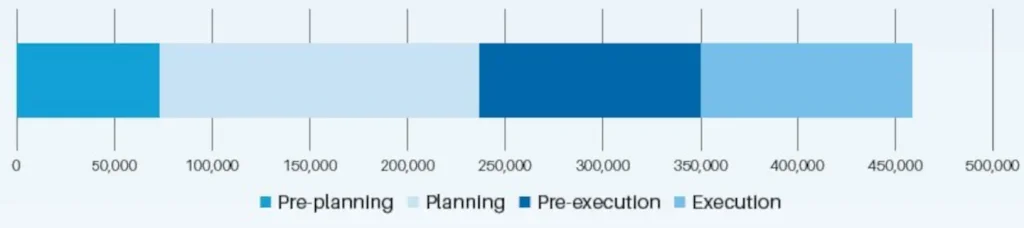

MENA – Industrial construction project pipeline

Value by stage ($ millions)

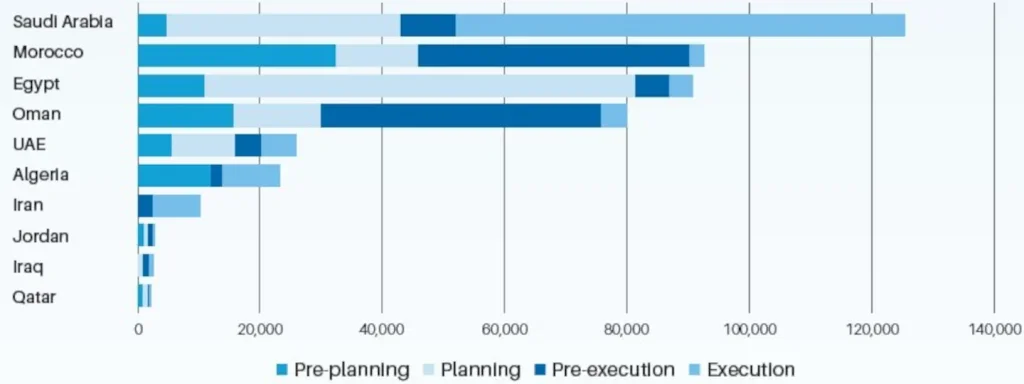

MENA – Industrial construction project pipeline

Value by stage and country ($ millions)

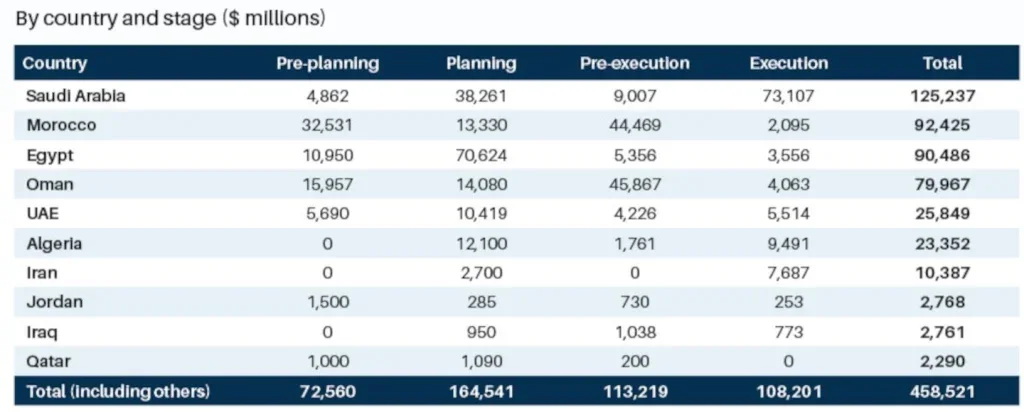

MENA – Industrial construction project pipeline

By country and stage ($ millions)

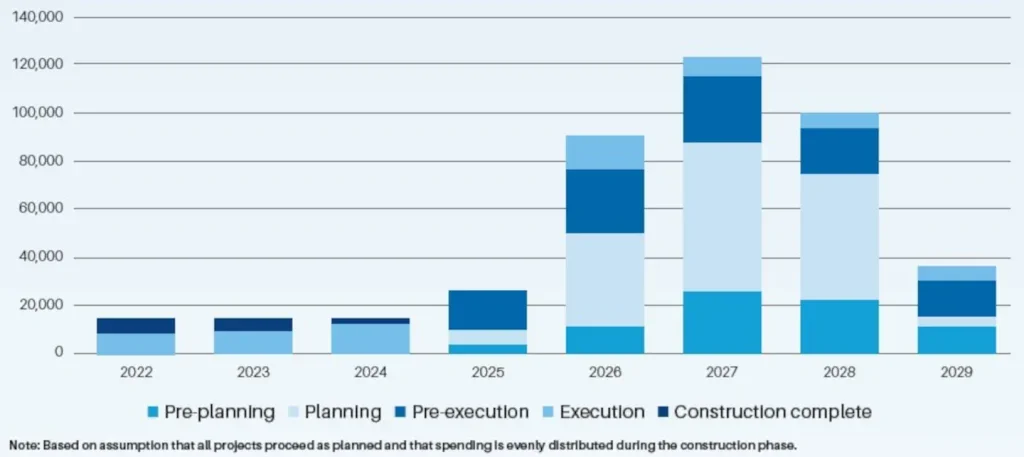

MENA – Industrial construction project pipeline, projected spending

Value by stage ($ millions)

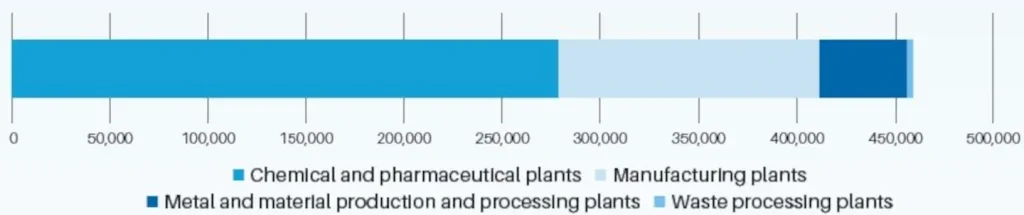

MENA – Industrial construction project pipeline

By sub-sectors ($ millions)

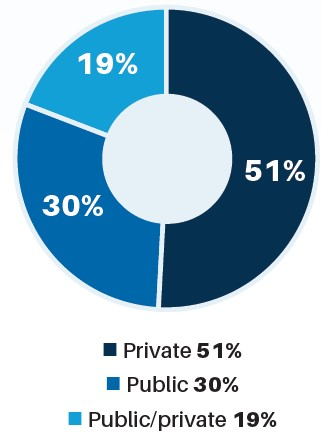

MENA – Industrial construction project pipeline

Funding mode (% of total)

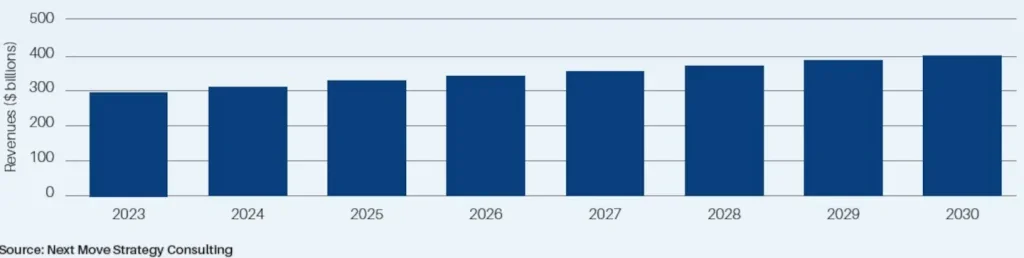

Middle East construction market revenue

2023–30

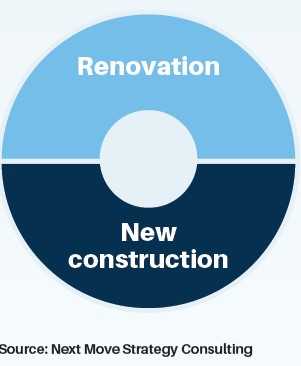

Middle East construction market segments

In the UAE, a joint venture between UAE and Moroccan investors – Dahamco – announced plans in December 2024 to invest nearly $25bn in a green hydrogen and ammonia project in Dakhla, a disputed territory in Western Sahara under Moroccan control. The first phase involves construction of product capacity, with an estimated $4bn investment, aiming for completion by 2031 with future phases rolling out every four to five years.

Elsewhere, Chinese steelmaker Hebei Xinfeng Steel revealed plans in December 2024 to invest $1.7bn in an industrial complex in Egypt. The project, spanning 3.8 million square meters, will be developed in two phases over the next five years.

According to GlobalData, the MENA region currently hosts an industrial construction pipeline valued at $458.5bn, spanning from project announcements through to execution. A slight majority – 51.7% or $237.1bn – remains in the early stages, including preplanning and planning. Saudi Arabia leads the region with the highest-value industrial project pipeline, totalling $125.2bn, of which $73.1bn relates to projects in the execution stage.

The largest project under development is the $54.9bn NEOM city: Oxagon. Currently in the execution phase, this futuristic development includes construction of industrial buildings, storage facilities and infrastructure works, commercial spaces and other associated facilities, all set for completion by 2030.